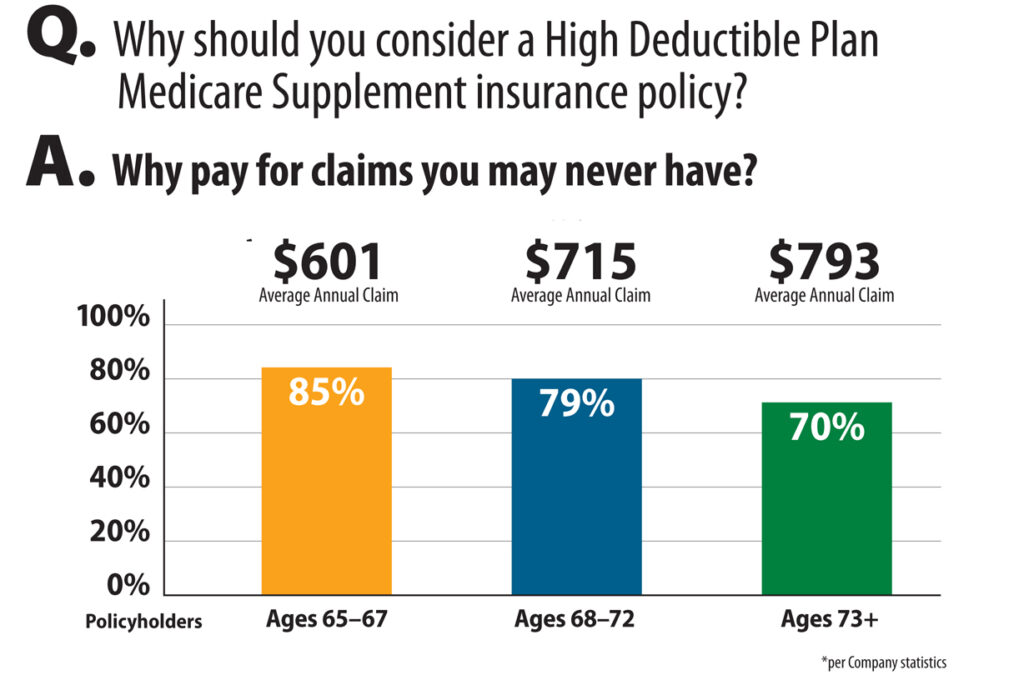

If you’re on a Medicare Supplement or considering a Medicare Supplement you might have noticed that supplement rates have gone up every year for the last three years. The reason that they have gone up is that Medicare raised all its deductibles and co-payments for Medicare Parts A and Part B. There is a solution to keep from paying the insurance companies thousands of dollars each year for services you are not using. I will try to explain an alternative that will lower your monthly premiums 75 percent or more of what you are currently paying, but before I do that let me give you the foundation for what I am about to show you. Look at the graphic below to see what the average claim paid out for supplements in 2021.

The above graphic shows the average amount one insurance company paid out for claims after Medicare paid what it was responsible for. I believe if you were to take all the insurance companies and run similar statistics they would all look about the same. The point being that if you are on a Medicare plan “F” or a Medicare plan “G” (which are the best Supplement plans), you are paying way more per year for services than need be espically if you are in good health.

The Solution

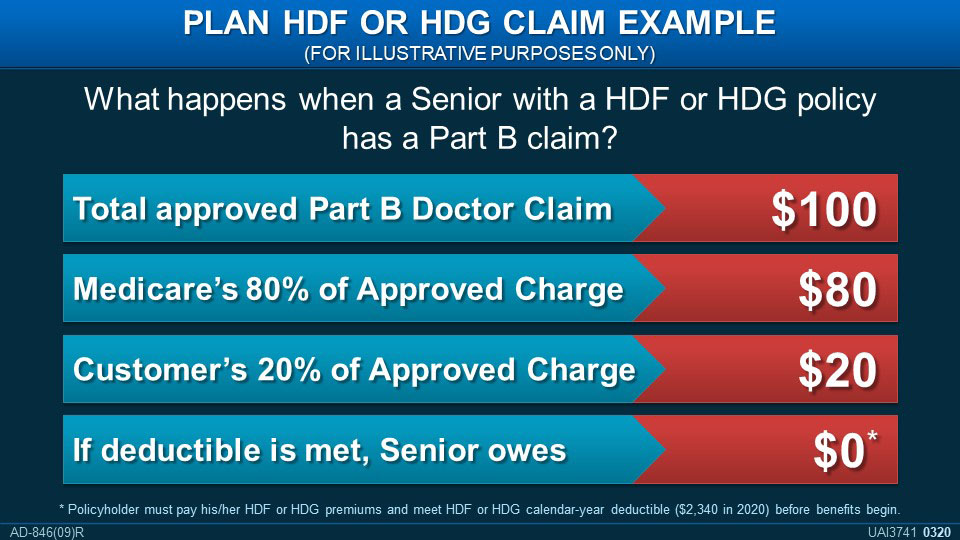

Is to purchase a HDF or HDG supplement. You may have not heard of a HDF or HDG supplement, that is because there are only a handful of companies that offer the HDF or HDG supplement. The HD stands for “High Deductible”, it is the maximum annual deductible you would have to pay out of pocket. After all copayments reach the deductible, Part A and Part B would be covered 100%, meaning that you would have no more out of pocket cost for the year. The annual deductible is set by the federal government and for 2023 is currently $2700. Below is an illustration of how the plan works.

In this example, say you go to visit your primary care physician and they charge $100 for the office visit. Medicare will pay 80% of the approved charges or in this case $80. In this example you would be responsible for 20% or $20. If your annual deductible had been met for the calendar year, you would owe “0”. If your deductible had not been met, you will be billed the $20, but everytime you would pay a copay it would go towards your deductible lowering it along the way throughtout the calendar year.

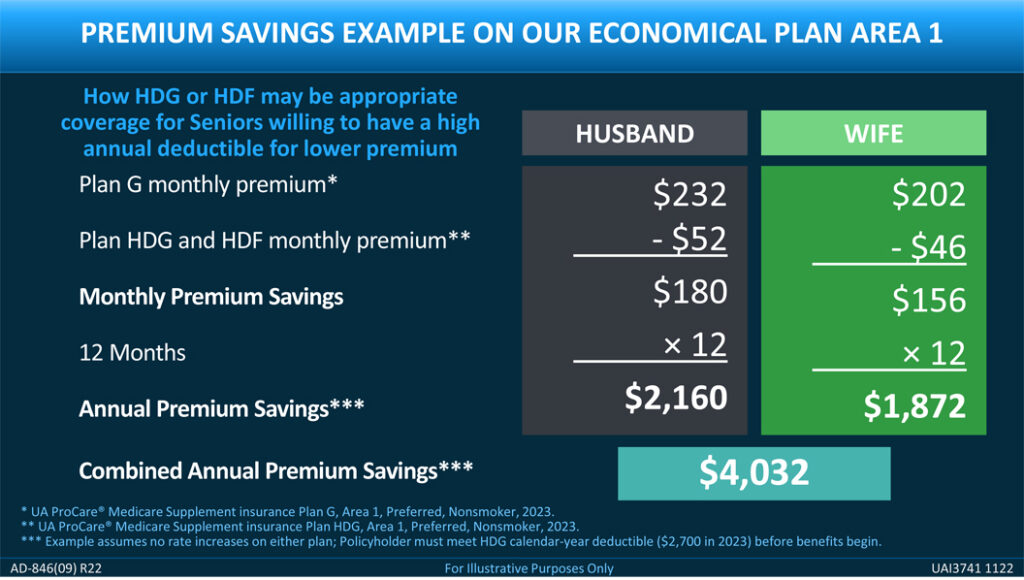

Below is an illustration of savings for a HDF and a HDG, These illustrations are based on a 65 year old male and female for area 1 in the state of Florida. Cost will vary depending upon where you live and your current age. If your in an area or at an age where your cost for supplements are more expensive, than your savings will be greater, but you will still save more than 70%.

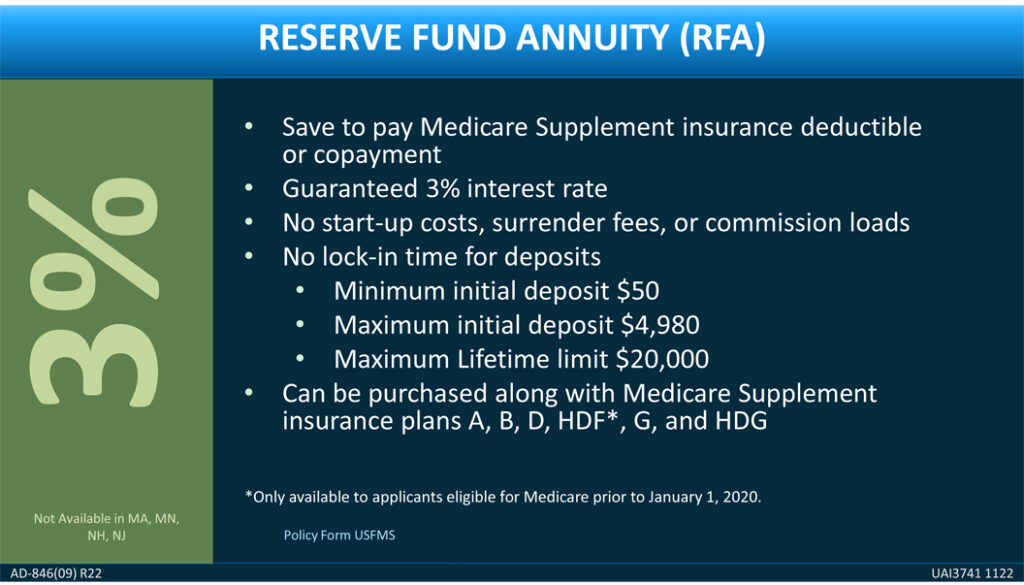

There is a way fund your annual deductible and earn 3% interest, it is called a reserve fund annuity.

How Does This Work?

You may elect to place funds into a Reserve Fund annuity to help pay for your calendar year deductible, copayment, or out-of-pocket limits. Funds can be deposited in a lump sum and/or through monthly deposits ($50 minimum) made with your insurance premium payments. When United American receives a healthcare provider’s claim and your calendar year deductible, copayment, or out-of-pocket limits amount has not been met, they will withdraw funds from your Reserve Fund and directly pay your deductible or copayment amount to the healthcare provider to the extent such funds exist in the Reserve Fund.

If the account balance in the Reserve Fund is not sufficient to pay the full amount owed to the healthcare provider, you will be responsible for paying any remaining balance directly to the healthcare provider. Once your calendar year deductible or copayment amount has been met, your insurance policy will begin paying all eligible benefits as outlined in the policy. Each quarter you will receive a statement of your annuity account balance.

There are no fees associated with the payment of deductible or copayment amounts or withdrawals from the accumulated annuity balance. All balances earn 3% interest and roll over from year to year. A maximum of $20,000 can be accumulated over a lifetime and goes to your beneficiaries if not used. Below is an explanation of the Reserve Fund Annuity.